Raising investment is tough, and closing the round is always massively stressful. That’s why deal dynamics are important.

A deal that seems ‘done and dusted’ suddenly fails. Everything was moving fast, and terms were agreed in principle. Out of the blue, everything reverts: investors start dragging your timeline, make unreasonable changes or new demands, and offer terms that are no longer standard nor fair. The list of tricks used is very long, and unless prepared, many founders fail at the final hurdle.

That’s why we teach a module named Deal Dynamics. It explains how founders can set (and keep) the pace, learn about power dynamics, and how to keep control of the process steps, timeline and other key milestones. We show how most investors will succumb to Fear Of Missing Out (FOMO) despite what they tell you and how founders can use information asymmetry: information is power, so use it.

Yes, as a founder, you must do many things right and also become a master at power plays, control mechanisms and deal-closing triggers. Every single founder should learn Deal Dynamics for life.

An amazing example is our alumni Henrik Hagemann, who recently announced Puraffinity’s $13.9 million in Series A funding, led by Octopus Ventures, one of the most prestigious funds in Europe. Hoping to close at $10 million, Hagemann mastered the round’s Deal Dynamics and leveraged it to negotiate terms, trigger FOMO, and close an oversubscribed round.

Here’s how he did it.

Preparation Builds Momentum

Considering the market downturn, we advised founders to plan for a longer fundraising process. Puraffinity went to market in November 2022 and closed the round on the 14th of June 2023, taking eight months in total. Although eight months is not the new norm yet – in the industry reports – it is the cautious thing to plan for.

During the Bootcamp, Hagemann clearly understood how much preparation he had to do before going to market. Luckily, they had bought some time with a grant and had enough runway to run a structured process.

Every document was prepared in advance — approach and introduction emails, summaries and in-person pitch decks, a fully detailed investor memorandum, financials, data room, etc, and a perfect-match list of target investors. By preparing in advance, they could build momentum, keeping investors engaged in every step of the process.

Finding the Right Investor Targets and Approaching Them

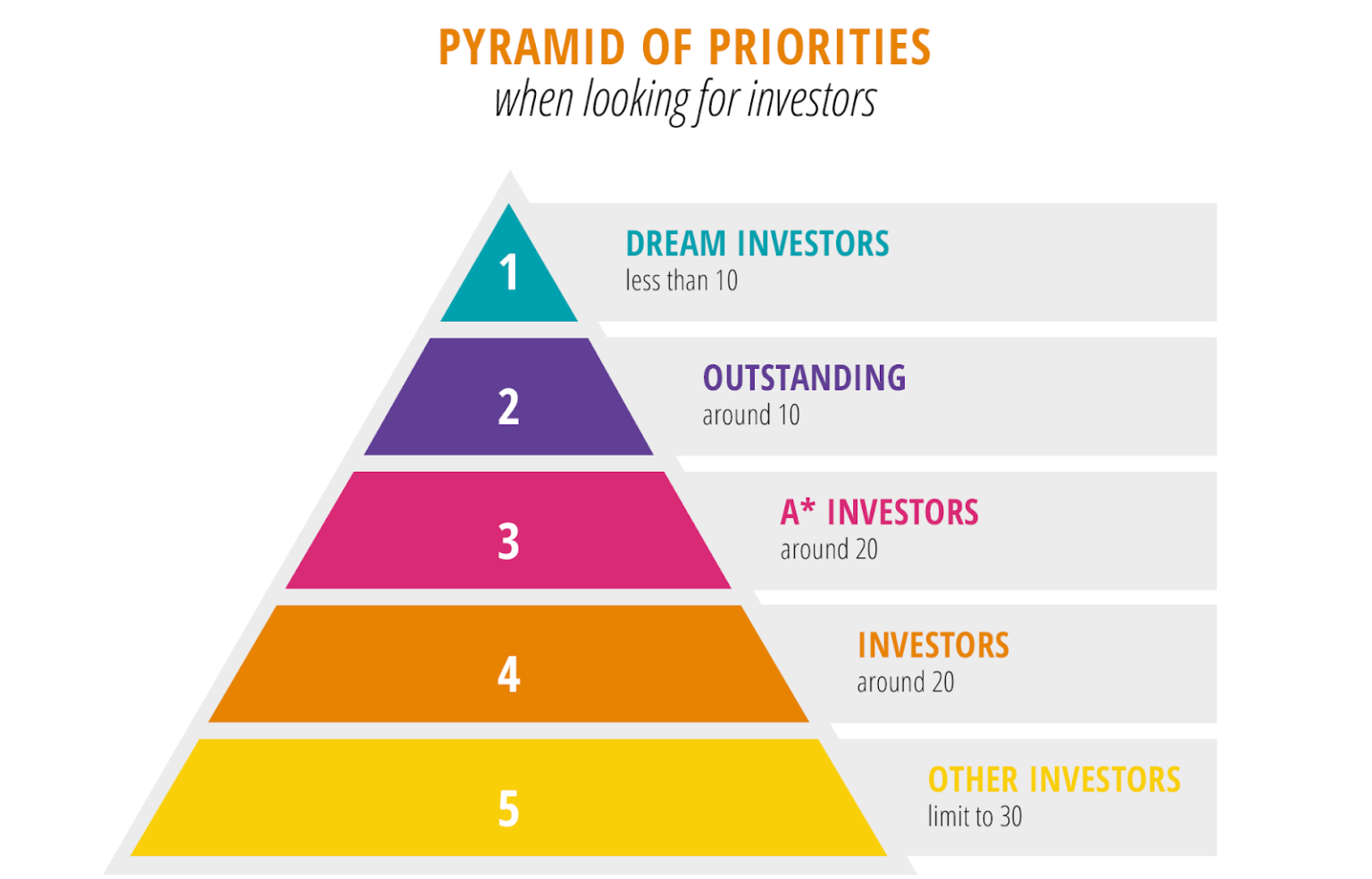

Henrik and his team listed 300+ funds that would qualify for their sector, geography and stage. The list was filtered and then organised using our Pyramid of Priorities methodology. After ranking them into separate tiers, it was clear who they needed to contact first, second, third, etc.

Henrik approached about 90 investors in total for this round. They got 35 rejections, 40 funds who completely ignored them, and about 15 who showed initial signs of interest in participating in the round.

How to organize your list of target investors following the Pyramid of Priorities, from dream investors to unknown and less familiar ones.

When they pressed play into their process and approached their Dream Investors, the responses came swiftly: in less than 24h, there were questions, requests for meetings, and a sense of momentum in the air. To Henrik’s surprise! “Francois said it would be quiet for a while”, he remembers. And he is right: we often say during Bootcamp that fundraising is a slow process, full of quiet and nothing until everything starts happening all at once. Well, not this time – kudos to Henrik for an amazing capacity to hook investors in early on!

Henrik was about to go on vacation, and although he had his follow-up emails ready, he thought he wouldn’t hear from anyone for weeks. With a personal commitment to replying to everyone within 24 hours, preparing all the documents in advance made a world of difference. A week after entering the market, Puraffinity already had meetings scheduled with some of their dream investors.

To manage his outreach, Henrik used (and improved!) our Bootcamp VC Tracker, a tool we use during the Bootcamp that really helps our alumni. The spreadsheet is meant to keep founders accountable while also helping them recognise feedback patterns, rejection, and success rates. Henrik even improved it by adding a probability scale for getting a deal based on the signs investors were showing with their probability to invest. Henrik reports this was particularly helpful for knowing when to prioritise the time and attention he would give to different investors.

Dealing with Meetings

It takes, on average, four to six meetings before a VC fund signs off on investing in a company. Multiply this by the number of investors you will be talking to, including those who might have one, two, or three meetings with you before saying no, and you’re in for a LONG ride.

For a green deep-tech company like Puraffinity, with a high-end research and production lab, it was important that some of these meetings were visits to their facilities – an investor even flew from Japan to the UK to see their lab (which scored high on his probability scale).

“We stand out in person; we have the space, team, office, and the lab they want to see.”

Hagemann scheduled his investor meetings tightly over two weeks, then took a week off to re-assess the entire process before diving into the next two weeks of meetings again and again. The pace was set: they would approach eight new investors, wait to see if they filled up their meeting slots, and if not, send a message to eight more investors until their 2-week calendar got filled out.

This schedule helped them focus on the investors they were already in conversation with while also keeping a pulse in the business. Knowing how bad the market was, many of those meetings happened in December. “We even flew directly from Singapore to London overnight to host onsite visits, which maybe wasn’t ideal, but had to be done. We were willing to sacrifice the comfort.”

Engender FOMO Amongst Investors

One of the first investors Puraffinity met with, a prestigious European VC fund in their space, was the first to offer a term sheet, wanting to take the whole round. Yup, the whole round. Even though the deal seemed good, Henrik learned during the Fundraising Bootcamp that competition is essential.

He returned to some of the Tier 1 investors on his list and leveraged that term sheet (without disclosing names), gently reminding other investors that the clock was ticking, “Hey, your fund needs to speed up if you want to join our round. There’s a fund interested in taking the whole thing”. No bluff, no ego, just facts and consistency in all communications. Founders who deliver on what they said before are impressive to investors.

Henrik knew better than to follow that term sheet: regardless of how good the deal might look, you should always trust the process. Keep competition in your fundraising round at all times. No exception, no deviation. No deal is guaranteed until you have cash in the bank.

Many VCs will claim all day that they are driven by conviction instead of FOMO, or justify their sudden interest as a desire to co-invest with other funds. Time and time again, we see that it’s not true, and that’s exactly how Henrik nudged other investors to accept his calendar and move faster with their own meetings, processes and term sheets. A process that goes to plan, on target and on time is very appealing to investors.

Term Sheets On The Table Aren’t The Finish Line

Another strategy within the realm of deal dynamics we recommend for all founders is to set a deadline before the start of the process to ensure investors don’t drag the process timeline for as long as they can (you get close to cashout and start accepting unsavoury terms you usually wouldn’t).

With his first term sheet in hand, Hagemann was able to set a deadline for all other interested investors. Not everyone can do this, but some founders use this fixed timeline strictly and effectively – see how Bootcamper Brittany Harriss used her tight fundraising timeline here.

After they sent out the final deadline, they got four term sheets within a few days (deal dynamics!). Unexpectedly, all funds interested wanted to lead the round.

With all the terms in hand and a good deal of competition between them, Puraffinity started negotiating valuations and terms.

Navigating Valuation and Negotiations

They leaned on another piece of advice gathered during the Fundraising Bootcamp, making investors name their price. “Does anyone truly know how to price this?” asked one investor.

Indeed, valuations in this sector and this market are anything but straightforward, and deal dynamics are essential when negotiating. In Puraffinity’s case, having multiple investors interested in leading the round led to even more complicated negotiations.

“We negotiated the price and the terms based on having competition. We told them, “We really like you. You’re a good partner. But they’re offering X and Y. Maybe we could try again a little bit harder?”

At a certain point, an investor directly asked, “Just tell us how much you want us to pay,” a question that founders should always push back on. It’s easier for investors to negotiate your price down (whatever it is) than to set a price fairly so they don’t lose the deal.

Founders, once the competition is set, you should always let them suggest the price.

Since Puraffinity wanted to grant the lead investor a seat at the board table, things got competitive. Attempting to create a syndicate involving multiple VCs leading the round turned into a complex dance of managing egos and preferences, eventually falling apart.

“We could have closed at the end of March, but we spent half of the month trying to syndicate the deal, looking for a way to have more than one VC lead the round”.

Ultimately, they opted for Octopus Ventures as the only lead investor. Puraffinity’s preferences were that the lead investor should be local, knowledgeable in this new sector, get a Board seat, require no more than 20-30% for the round, and be available frequently.

Learnings from Puraffinity’s Series A round

Intros Are Powerful – Use Them Well

Networking played a significant role in Puraffinity’s fundraising journey – about 50% of the contacts came from shareholders, and a bit less than 50% from their own team. They sat together and prepared a list with everyone in their ecosystem, working individually to find who could introduce them to what kinds of funds. Out of the people they talked to, less than 20% were approached with cold emails.

Puraffinity has a complex product, so it was useful to use Bootcamp’s forwardable email technique, preventing introductory parties from having to explain what they do. Luckily, during the Bootcamp, we had already worked quite a bit on simplifying their product and USP. They invested even more time to achieve their intro goals, finding metaphors to make their solution easy and interesting to grasp.

“At some point, we came up with something like “We make sustainable materials that take out the nasties in water”, and people were like “oh okay, I don’t want nasties in my water”. We still had to explain what those nasties meant, so we had to continue simplifying.”

Mindset shift

After joining the Bootcamp, Henrik decided to work with a coach to stop, in his words, “his tendencies of being a people-pleaser”, a trait that could be a BIG disadvantage in fundraising. Our approach is quite bold in many ways, as we teach founders to set terms that work for them, not just for the investors. Henrik realised he would need a nudge to interact with investors confidently rather than just agreeing to their demands.

Be physically and emotionally prepared

Henrik was still managing some of the operations while fundraising, which put him close to burnout – a scenario too familiar in the startup world. The stress can also be hard on most founders, and he fell ill multiple times during the process.

Remember the holiday Henrik was about to go on when investors showed initial signs of interest? He had a few important meetings in his rental car – the only spot with decent wifi – balancing everything while on holiday in Italy. Not knowing that the process would pick up pace so quickly was definitely an oversight.

Our recommendation during the Bootcamp resonated strongly: single focus. Fundraising is a full-time job, you can’t run it as a side gig. Henrik agrees. “Next time, I will take someone from the leadership team to focus on the business while I do the fundraising”.

And perhaps consider booking some holidays before you start the process!

Look Beyond the Term Sheet

The term sheet might look good, but the real deal is the people behind it. In Henrik’s words, “Shiny term sheet, not-so-shiny investors”. Due diligence is such a critical part of fundraising that you must filter out the kind of funds you don’t want to be ‘married’ with.

Be Prepared to Raise

Take the process seriously for a real chance to reach your fundraising target. Henrik said they got lucky when Puraffinity raised their Seed round. Even though they had a good round, many mistakes were made, and everything was a bit improvised. It would have been impossible to succeed in Series A following the same path and without knowing the importance of deal dynamics, which made him thankful for the decision to join Bootcamp.

“If I had done what I did raising Series A during our Seed round, it wouldn’t have worked out, investors would have laughed at us. It definitely helped me take the process more seriously.”

The Outcome

Puraffinity’s Seed investors also joined their Series A, showing they were happy with their initial investment. When your previous investors want in again, it’s a big green flag for new ones.

The company aimed for a $10 million raise. Their stellar preparation, focus and control of deal dynamics landed at $13.9 million, led by Octopus Ventures, a non-specialist and one of the most prestigious funds in Europe. Henrik swears he will follow the same playbook for their Series B round.

Best of all (and as we teach at the Bootcamp), investors who weren’t selected for the round already applied to the next one – a classic.

Puraffinity’s Series A round is a great story of how being prepped can pivot your fundraising journey from a game of chance to a laser-focused win.

Companies might raise funds without the prep we offer during the Bootcamp, of course, but they’re counting on a lot of luck. And in today’s environment, that’s one strategy we cannot support. There is a better way, using deal dynamics and many other strategies, and our alumni have been showing this time and time again.

No one was born a fundraiser, but our programme is a game changer if you want to succeed and raise the cash your company needs.