If you’ve been invited to pitch to VC investors, chances are you’re focused on preparing your pitch. There’s no doubt you should invest a significant amount of time in doing this, whether you’re working on a comprehensive pitch deck or getting ready to pitch without slides.

However, in doing so, we see many founders fall into a trap. They forget that the pitch is far from the whole story when it comes to securing VC funding. Consequently, they neglect other aspects of the founder-investor conversation that are just as crucial (if not more so). The result? They come away with nothing.

Here are the mistakes we see entrepreneurs make time and time again – and what you can do to avoid them.

Mistake 1: Failing to articulate the ask clearly

You’d be amazed how many founders get this wrong. Far too many go into a pitch without a clear “why”, “who”, “when” or even “how much”! Approaching a conversation with investors with an attitude of “I just need money” is a surefire way to get precisely nowhere.

Here’s what you need to communicate in detail – with headline numbers and maximum clarity – when it comes to your ask of investors:

● The amount of investment you’re seeking ● How you arrived at this number (be sure to include details of your burn, what it’s comprised of and your runway) ● Where the funds will go if you secure them ● Your timeline for using the funds ● Your contingency

Mistake 2: Failing to prepare for the post-pitch Q&A

Picture the scene: you’ve spent endless hours preparing your pitch and you deliver it flawlessly. You’ve stayed within the three-minute time limit and the judges’ applause gives your ego a huge boost. You open the floor for questions and then…it all goes horribly wrong.

This is the part of the pitch that so many founders forget to prepare for. Others make the mistake of thinking that they can answer investors’ questions simply by referring to their trusty slide deck.

Now, if you’ve put the work into your pitch, the answers to the questions that investors ask in the Q&A will almost certainly be in there. It’s a given that you’ll need to repeat the information in the pitch – without displaying any frustration or impatience – but you have to be able to show that you know your stuff without having to default to a slide deck or script.

You also need to be able to talk about your company and your bid for investment confidently, naturally and in detail, no matter how the investors frame their questions.

The good news is that the questions that investors will ask you are already out there. Just watch a handful of Demo Day videos and you’ll see that the questions are always the same.

Make a note of everything that comes up and once you’ve got your list, start developing your answers and then learning them.

To hit the mark, your answers should be simple, short and honest. Wherever possible, you should support them with a number. If you don’t have one you can share, avoid the temptation to make one up or attempt to provide an explanation. “We don’t have that number nailed down yet” is a perfectly valid answer.

Mistake 3: Failing to prepare properly for post-pitch meetings

Now picture another scene: the investors like your pitch and you wow them in the Q&A. You’re delighted when they invite you to a follow-up conversation. You enter the meeting feeling confident and positive but leave with nothing. No encouraging feedback and no invite to that all-important next meeting.

So what went wrong? In all likelihood, you didn’t prepare properly for the conversation. Investors demand that you’re on top of your game in meetings, and that you know your company and industry inside out. At the end of the day, they invest only in the very best companies. So do your homework and make sure you can talk about the following areas (to name just a few) eloquently, with no hesitation:

● Your previous month’s numbers ● Your top three customers ● Your industry competitors

Many founders have learned the hard way that there are no second chances in funding circles. You’ll only get one shot with your dream investor – so don’t blow it!

Mistake 4: Failing to ask questions

It’s no exaggeration to describe the founder-investor relationship as a marriage of sorts. As a result, it’s vital for founders to due diligence investors, just as investors take time and care to research the founders and companies they invest in.

Ultimately, investors expect you to have questions. In fact, it’s highly likely to count against you if you don’t. After all, why wouldn’t you want to know more about a potential investor’s background or about the fund itself?

Here are some of the areas in which investors will expect you to demonstrate an interest:

● Their background ● Their achievements ● How they can help you ● When the investors set the fund up ● How many investments they’ve made so far ● Whether they’ve already received the funds they’re offering to invest

As part of your pitch preparation – and your preparation for any subsequent meetings — plan a set of questions that you can ask fluidly and naturally as the conversation unfolds. Don’t find yourself in the dangerous position of having to come up with questions on the spot.

Ready to learn more?

If you’re preparing to raise VC investment, we’ll teach you how to avoid these mistakes and countless more in our programme, the Fundraising Bootcamp.

It’s not your typical fundraising class. You’ll learn how to win investment for your startup or scale-up live, with coaching from those who’ve done it. Check out our upcoming cohorts and let’s see if we’re a good fit.

Raising investment is tough, and closing the round is always massively stressful. That’s why deal dynamics are important.

A deal that seems ‘done and dusted’ suddenly fails. Everything was moving fast, and terms were agreed in principle. Out of the blue, everything reverts: investors start dragging your timeline, make unreasonable changes or new demands, and offer terms that are no longer standard nor fair. The list of tricks used is very long, and unless prepared, many founders fail at the final hurdle.

That’s why we teach a module named Deal Dynamics. It explains how founders can set (and keep) the pace, learn about power dynamics, and how to keep control of the process steps, timeline and other key milestones. We show how most investors will succumb to Fear Of Missing Out (FOMO) despite what they tell you and how founders can use information asymmetry: information is power, so use it.

Yes, as a founder, you must do many things right and also become a master at power plays, control mechanisms and deal-closing triggers. Every single founder should learn Deal Dynamics for life.

An amazing example is our alumni Henrik Hagemann, who recently announced Puraffinity’s $13.9 million in Series A funding, led by Octopus Ventures, one of the most prestigious funds in Europe. Hoping to close at $10 million, Hagemann mastered the round’s Deal Dynamics and leveraged it to negotiate terms, trigger FOMO, and close an oversubscribed round.

Here’s how he did it.

Preparation Builds Momentum

Considering the market downturn, we advised founders to plan for a longer fundraising process. Puraffinity went to market in November 2022 and closed the round on the 14th of June 2023, taking eight months in total. Although eight months is not the new norm yet – in the industry reports – it is the cautious thing to plan for.

During the Bootcamp, Hagemann clearly understood how much preparation he had to do before going to market. Luckily, they had bought some time with a grant and had enough runway to run a structured process.

Every document was prepared in advance — approach and introduction emails, summaries and in-person pitch decks, a fully detailed investor memorandum, financials, data room, etc, and a perfect-match list of target investors. By preparing in advance, they could build momentum, keeping investors engaged in every step of the process.

Finding the Right Investor Targets and Approaching Them

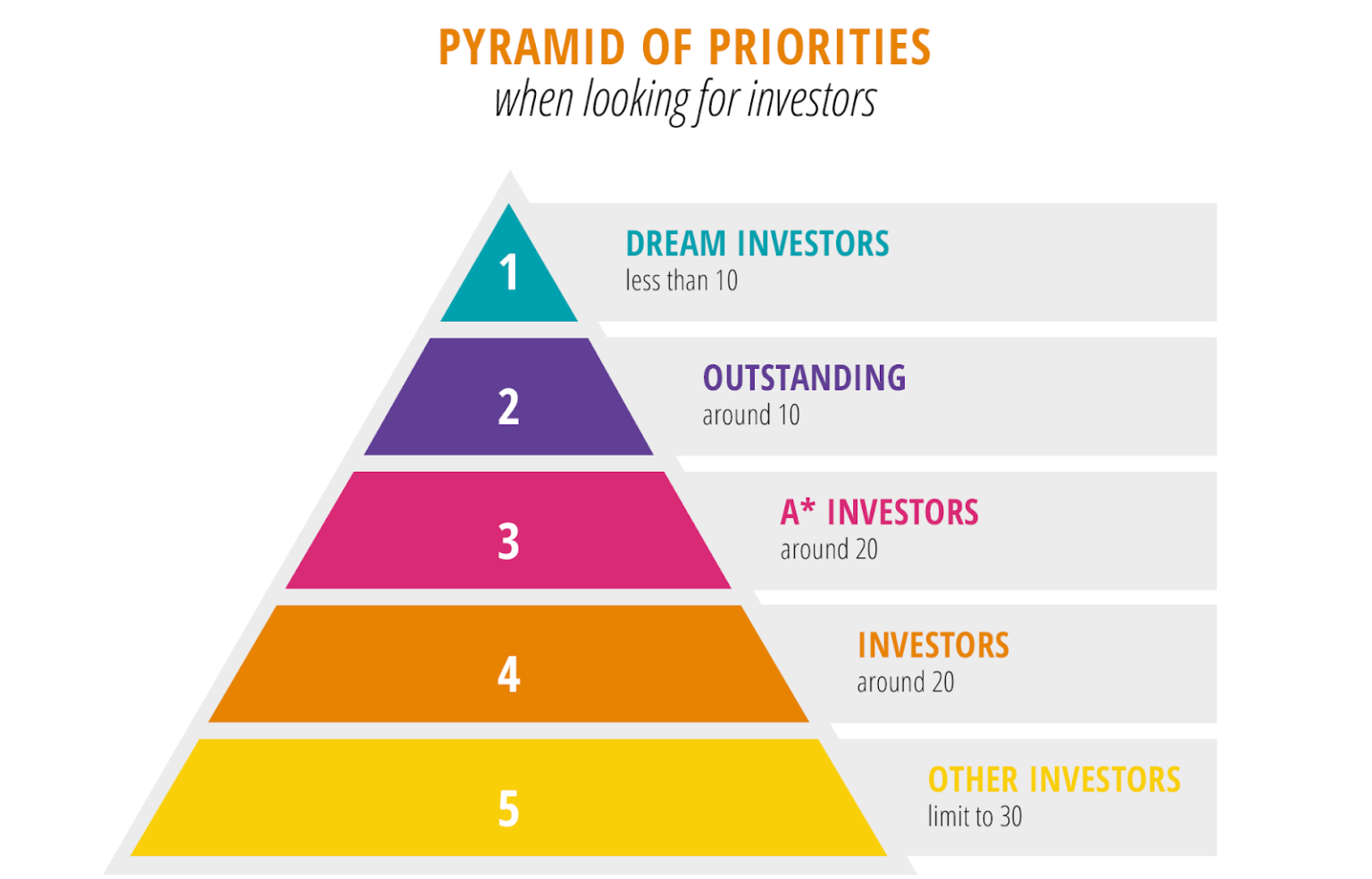

Henrik and his team listed 300+ funds that would qualify for their sector, geography and stage. The list was filtered and then organised using our Pyramid of Priorities methodology. After ranking them into separate tiers, it was clear who they needed to contact first, second, third, etc.

Henrik approached about 90 investors in total for this round. They got 35 rejections, 40 funds who completely ignored them, and about 15 who showed initial signs of interest in participating in the round.

How to organize your list of target investors following the Pyramid of Priorities, from dream investors to unknown and less familiar ones.

When they pressed play into their process and approached their Dream Investors, the responses came swiftly: in less than 24h, there were questions, requests for meetings, and a sense of momentum in the air. To Henrik’s surprise! “Francois said it would be quiet for a while”, he remembers. And he is right: we often say during Bootcamp that fundraising is a slow process, full of quiet and nothing until everything starts happening all at once. Well, not this time – kudos to Henrik for an amazing capacity to hook investors in early on!

Henrik was about to go on vacation, and although he had his follow-up emails ready, he thought he wouldn’t hear from anyone for weeks. With a personal commitment to replying to everyone within 24 hours, preparing all the documents in advance made a world of difference. A week after entering the market, Puraffinity already had meetings scheduled with some of their dream investors.

To manage his outreach, Henrik used (and improved!) our Bootcamp VC Tracker, a tool we use during the Bootcamp that really helps our alumni. The spreadsheet is meant to keep founders accountable while also helping them recognise feedback patterns, rejection, and success rates. Henrik even improved it by adding a probability scale for getting a deal based on the signs investors were showing with their probability to invest. Henrik reports this was particularly helpful for knowing when to prioritise the time and attention he would give to different investors.

Dealing with Meetings

It takes, on average, four to six meetings before a VC fund signs off on investing in a company. Multiply this by the number of investors you will be talking to, including those who might have one, two, or three meetings with you before saying no, and you’re in for a LONG ride.

For a green deep-tech company like Puraffinity, with a high-end research and production lab, it was important that some of these meetings were visits to their facilities – an investor even flew from Japan to the UK to see their lab (which scored high on his probability scale).

“We stand out in person; we have the space, team, office, and the lab they want to see.”

Hagemann scheduled his investor meetings tightly over two weeks, then took a week off to re-assess the entire process before diving into the next two weeks of meetings again and again. The pace was set: they would approach eight new investors, wait to see if they filled up their meeting slots, and if not, send a message to eight more investors until their 2-week calendar got filled out.

This schedule helped them focus on the investors they were already in conversation with while also keeping a pulse in the business. Knowing how bad the market was, many of those meetings happened in December. “We even flew directly from Singapore to London overnight to host onsite visits, which maybe wasn’t ideal, but had to be done. We were willing to sacrifice the comfort.”

Engender FOMO Amongst Investors

One of the first investors Puraffinity met with, a prestigious European VC fund in their space, was the first to offer a term sheet, wanting to take the whole round. Yup, the whole round. Even though the deal seemed good, Henrik learned during the Fundraising Bootcamp that competition is essential.

He returned to some of the Tier 1 investors on his list and leveraged that term sheet (without disclosing names), gently reminding other investors that the clock was ticking, “Hey, your fund needs to speed up if you want to join our round. There’s a fund interested in taking the whole thing”. No bluff, no ego, just facts and consistency in all communications. Founders who deliver on what they said before are impressive to investors.

Henrik knew better than to follow that term sheet: regardless of how good the deal might look, you should always trust the process. Keep competition in your fundraising round at all times. No exception, no deviation. No deal is guaranteed until you have cash in the bank.

Many VCs will claim all day that they are driven by conviction instead of FOMO, or justify their sudden interest as a desire to co-invest with other funds. Time and time again, we see that it’s not true, and that’s exactly how Henrik nudged other investors to accept his calendar and move faster with their own meetings, processes and term sheets. A process that goes to plan, on target and on time is very appealing to investors.

Term Sheets On The Table Aren’t The Finish Line

Another strategy within the realm of deal dynamics we recommend for all founders is to set a deadline before the start of the process to ensure investors don’t drag the process timeline for as long as they can (you get close to cashout and start accepting unsavoury terms you usually wouldn’t).

After they sent out the final deadline, they got four term sheets within a few days (deal dynamics!). Unexpectedly, all funds interested wanted to lead the round.

With all the terms in hand and a good deal of competition between them, Puraffinity started negotiating valuations and terms.

Navigating Valuation and Negotiations

They leaned on another piece of advice gathered during the Fundraising Bootcamp, making investors name their price. “Does anyone truly know how to price this?” asked one investor.

Indeed, valuations in this sector and this market are anything but straightforward, and deal dynamics are essential when negotiating. In Puraffinity’s case, having multiple investors interested in leading the round led to even more complicated negotiations.

“We negotiated the price and the terms based on having competition. We told them, “We really like you. You’re a good partner. But they’re offering X and Y. Maybe we could try again a little bit harder?”

At a certain point, an investor directly asked, “Just tell us how much you want us to pay,” a question that founders should always push back on. It’s easier for investors to negotiate your price down (whatever it is) than to set a price fairly so they don’t lose the deal.

Founders, once the competition is set, you should always let them suggest the price.

Since Puraffinity wanted to grant the lead investor a seat at the board table, things got competitive. Attempting to create a syndicate involving multiple VCs leading the round turned into a complex dance of managing egos and preferences, eventually falling apart.

“We could have closed at the end of March, but we spent half of the month trying to syndicate the deal, looking for a way to have more than one VC lead the round”.

Ultimately, they opted for Octopus Ventures as the only lead investor. Puraffinity’s preferences were that the lead investor should be local, knowledgeable in this new sector, get a Board seat, require no more than 20-30% for the round, and be available frequently.

Learnings from Puraffinity’s Series A round

Intros Are Powerful – Use Them Well

Networking played a significant role in Puraffinity’s fundraising journey – about 50% of the contacts came from shareholders, and a bit less than 50% from their own team. They sat together and prepared a list with everyone in their ecosystem, working individually to find who could introduce them to what kinds of funds. Out of the people they talked to, less than 20% were approached with cold emails.

Puraffinity has a complex product, so it was useful to use Bootcamp’s forwardable email technique, preventing introductory parties from having to explain what they do. Luckily, during the Bootcamp, we had already worked quite a bit on simplifying their product and USP. They invested even more time to achieve their intro goals, finding metaphors to make their solution easy and interesting to grasp.

“At some point, we came up with something like “We make sustainable materials that take out the nasties in water”, and people were like “oh okay, I don’t want nasties in my water”. We still had to explain what those nasties meant, so we had to continue simplifying.”

Mindset shift

After joining the Bootcamp, Henrik decided to work with a coach to stop, in his words, “his tendencies of being a people-pleaser”, a trait that could be a BIG disadvantage in fundraising. Our approach is quite bold in many ways, as we teach founders to set terms that work for them, not just for the investors. Henrik realised he would need a nudge to interact with investors confidently rather than just agreeing to their demands.

Be physically and emotionally prepared

Henrik was still managing some of the operations while fundraising, which put him close to burnout – a scenario too familiar in the startup world. The stress can also be hard on most founders, and he fell ill multiple times during the process.

Remember the holiday Henrik was about to go on when investors showed initial signs of interest? He had a few important meetings in his rental car – the only spot with decent wifi – balancing everything while on holiday in Italy. Not knowing that the process would pick up pace so quickly was definitely an oversight.

Our recommendation during the Bootcamp resonated strongly: single focus. Fundraising is a full-time job, you can’t run it as a side gig. Henrik agrees. “Next time, I will take someone from the leadership team to focus on the business while I do the fundraising”.

And perhaps consider booking some holidays before you start the process!

Look Beyond the Term Sheet

The term sheet might look good, but the real deal is the people behind it. In Henrik’s words, “Shiny term sheet, not-so-shiny investors”. Due diligence is such a critical part of fundraising that you must filter out the kind of funds you don’t want to be ‘married’ with.

Be Prepared to Raise

Take the process seriously for a real chance to reach your fundraising target. Henrik said they got lucky when Puraffinity raised their Seed round. Even though they had a good round, many mistakes were made, and everything was a bit improvised. It would have been impossible to succeed in Series A following the same path and without knowing the importance of deal dynamics, which made him thankful for the decision to join Bootcamp.

“If I had done what I did raising Series A during our Seed round, it wouldn’t have worked out, investors would have laughed at us. It definitely helped me take the process more seriously.”

The Outcome

Puraffinity’s Seed investors also joined their Series A, showing they were happy with their initial investment. When your previous investors want in again, it’s a big green flag for new ones.

The company aimed for a $10 million raise. Their stellar preparation, focus and control of deal dynamics landed at $13.9 million, led by Octopus Ventures, a non-specialist and one of the most prestigious funds in Europe. Henrik swears he will follow the same playbook for their Series B round.

Best of all (and as we teach at the Bootcamp), investors who weren’t selected for the round already applied to the next one – a classic.

Puraffinity’s Series A round is a great story of how being prepped can pivot your fundraising journey from a game of chance to a laser-focused win.

Companies might raise funds without the prep we offer during the Bootcamp, of course, but they’re counting on a lot of luck. And in today’s environment, that’s one strategy we cannot support. There is a better way, using deal dynamics and many other strategies, and our alumni have been showing this time and time again.

No one was born a fundraiser, but our programme is a game changer if you want to succeed and raise the cash your company needs.

Unspoken tricks that work & the power of Deal Dynamics

You spent months preparing your investor proposition, your financial model and your investor pack. You crafted a list of relevant investors, killed your fears, jumped in and went pitching investors. You received the usual “you’re great, a bit too early, come back later, send us updates please” and “oh, uhhh, well, no, but maybe later” and other rejections every founder learns to receive.

You still managed to pull it off through sheer grit and get one or two investors interested – congrats! Closing your funding round is, finally, within sight.

And then all hell breaks loose.

Investors change the tone, and deadlines get dragged out, last minute ‘investor friendly’ terms appear and become deal breakers, you get asked to disclose information you shouldn’t, told to drop X or Y investor, as they make ‘suggestions’ (not really optional) and add their conditions.

Let me tell you: this deal isn’t closing anytime soon. You’ve lost it and will struggle to close it on good terms.

They won the game – a common occurrence, especially today when deals are slower, investors more demanding, and all their dirty tricks considered “fair game” again.

How, why? What did you miss?

We have helped hundreds of founders through their funding rounds, and one of the most stressful times is… right at the end. When you think it’s all sewn up and about to close. Many (realistically, most) untrained founders and CEOs fail right there, at the last hurdle, the last lap when the finish line is in plain view.

This is when you need to understand Deal Dynamics. I’m no psychologist, but I learnt (the hard way, at great cost) that once you understand the psychology behind the power play, control mechanisms and deal-closing triggers, you win.

You close your funding round on your terms, not theirs.

Your calendar, not theirs.

With less stress and blowup risk.

Understand the Human Behind the Money

Guess what, investors are human beings, too – no, really, I mean it, they are!

They have egos (some of them supersized), cash deployment timings and ownership goals, and a partnership to report to (internal politics are rife), with their LPs (investors) asking why they lost that deal and this other one when other fund XYZ closed. Lose too many hot deals, and “maybe entrepreneurs don’t value you that much”.

Tips For Navigating Investor Deal Dynamics

How to engender FOMO

Every investor I know repeatedly tells me other VCs’ deals don’t impact theirs, then lists them alphabetically, with dates and values, within minutes. LOL.

2. FOLS (Fear of Looking Stupid)

Even greater than FOMO, by some margin.

It’s okay for investors to pass on a deal. What it’s not okay for them is to be dropped by the founder in the finals. So you, the founder, can control the final lap of your funding round, who’s investing and who’s not. Deal-closing uncertainty is your friend.

3. Fundraising is a game of Information Asymmetry

VCs always request (sometimes forcefully) way more information than is reasonable without ever giving any indication of interest. Pro poker-faced players. Learn how to counter that.

4. Disclosures matter. A Lot.

Understand how and when to release each set of info.

Exclusivity is luxury. Price it accordingly. Investors need information, which you should disclose, but keeping some information to yourself can trigger their FOLS. Use it appropriately, and they fold.

5. Keeping to your timeline and deadlines at all times

Master it, as they read it, as a strong signal of strength and change their process dates and priorities accordingly. If you don’t do it, they’ll play the clock against you, and when time runs out, you will accept terrible terms you shouldn’t. Options vs. Timings. Read this story here.

6. It’s your business. Your shares. Your timing.

Your cash requirement, your business. You issue the deal terms (use our templates; they are fair to both sides). You decide when you accept offers, and you choose the investors. You drive. It’s remarkably easy once you know how.

Ready to deep-dive into the deal dynamics of fundraising?

Learn how to build FOMO, FOLS, leverage egos, navigate exclusivity periods, disclosures and hidden names, and even have a plan B. This is one of the multiple sessions we cover during our programme, the Fundraising Bootcamp.

We’re not your typical fundraising class. And we can help you close your funding round – from seed to Series C. Check out our next programmes here, and let’s see if we’re a good fit.

Ah, the mystical realm of Venture Capital and Venture Capitalists- the enigmatic beings who hold the keys to startup money. We often talk about VCs as if they’re distant, mythical entities with minds so hard to crack we can’t help but feel intimidated by them.

Reality check: VCs are just like us founders; they want (and need) promising startup founders to succeed and grow big. And to figure this out, they need to understand you deeply. That’s why the pitch matters so much – if you cannot communicate what you do in a simple, comprehensive, yet exciting way, you end up on the ‘meeeeh‘ pile along with the other 2,000+ CEOs they meet that year.

The knowledge to crack the Venture Capital code comes from actual experience

You only get one shot at this; there’s no second chance or iteration. Be knowledgeable and casually demonstrate that magic mix of IQ, team (EQ) and numbers – you’re in. Or end up on the pile. So many have amazing tech but don’t understand Venture Capital, the process, the narrative they need, or how to demonstrate how good they are (hint: not their product).

That’s why we created our programme. To stop great companies and founders from being bypassed for the wrong reasons. The knowledge to crack the Venture Capital code comes from actual experience, not blogs or wishlists. We’ve raised, invested, built, worked in investment banking and sat on all sides of the table. We share it with articles around here and on our LinkedIn, too.

But let’s do something different.

This time, we’ll let VCs do the talking – not because they know something we don’t, but to show you that what we teach is truly industry-insider knowledge of Venture Capital. We’re not teaching theory or anything academic; these recommendations have been part of our curriculum all along, and they match exactly what investors do and say.

Let’s dive into the core of VC-Founder dynamics – where wisdom meets wits.

Make investors feel FOMO

Ego-driven VCs will claim all day that they don’t check out other investors and have no FOMO (Fear of Missing Out). We see, time and time again, that it’s not true, and we built the tools, process and proprietary methodology to unleash it among potential investors – our alumni repeatedly proved that this tactic simply works, especially once they’ve won the first investor/s.

Picture this: a founder methodically (and tirelessly) approaches one VC after another using our Pyramid of Priorities strategy in an enormous uphill battle. Most investors reply by…ghosting them. One day, a relevant VC (industry specialist, reputation, brand) shows interest, and everything changes.

“If fund XYZ is investing, that’s good enough a signal for me”.

The ghosty investors suddenly get very eager to engage, request meetings, and state their undying love of the company. FOMO. As Dan said, “Finding the anchor unlocks the next“. Like magic!

We’ve been saying this all along: you never truly know what kind of experience a VC has in your industry (if any) or what terminology they’re comfortable with. Use jargon at your own peril; usually, all you achieve is to alienate good potential investors who aren’t specialists and make them feel like idiots.

We call it the grandma test (and thank you, Alexis, for confirming!). When pitching to investors, you want to tell the most clear and compelling story you can, leaving them wanting more. Instead, most founders bury their goodness in complexity and complicated lingo or visuals. Alexis said it best: Explain the problem you’re solving so that even a five-year-old could understand.

In today’s market, investors have all the incentives to take their time and explore multiple options before committing, dragging your timeline with them. When you set a deadline, you give investors a reason to act promptly or be out – no more time wasters. It allows those genuinely interested to jump on board, run their process + due diligence, and move forward with conviction. The others are just trying to string you, waiting for you to run out of cash and accept unfavourable terms.

Bootcampers will know we are big on having a strict timeline. And it looks like we’re not the only ones who believe this. The only thing we disagree with is that 10 days is too short, in our opinion. Good investors have other deals in process, so respect their time too.

VC funding is the most complex form of capital you can raise. Criticise all you want, search for alternative funding sources (there are plenty, thankfully – we also show you all eight categories, with names and direct links), or cross your fingers and hope for the best.

Or you can learn how the game works, the nasty terms you will likely be offered and how to avoid them. Many CEOs are first-time founders with zero or little fundraising experience, while investors do deals day in and day out. Knowledge is what can keep you safe out there.

At the Fundraising Bootcamp, we don’t believe in decks as the Internet tells you. Your pitch is only bait, and you should consider it as such, nothing more. It is designed to let you express, without referring to any slides, clarity, excitement, numbers/potential and, more than anything else, must make investors keen to know more.

To do that, they ask for a follow-up meeting. Period. Strip the deck out of over-the-top explanations about your vision, mission, product, tech maps, founder’s love story, etc. The deck answers some basic questions: Investors seek concrete data and numbers. They’re looking for your team. They need to know if your market is big enough, and if you have enough traction, and they usually spend most of their time on your financials. There are other items you must display, even if they don’t ask you for them.

And there you go! Five times, investors validated what we teach thoroughly at Bootcamp. If you’re unsure how to act on this advice, you should join one of our cohorts. We have the playbook and can help you nail your next round.

Click here for more info, see where our next programme runs, and don’t take our word for it. Check out our wall of CEO reviews instead.

A Deep Dive into the Fundraising Bootcamp Alumna’s Strategy and Lessons Learned

It hasn’t been easy for startups in 2023 – especially if they need cash. After the 2021 overbidding frenzy, valuations have returned to more realistic levels, and fundraising activity has slowed down. It has been a year of mostly flat rounds, with investors and startups taking a “wait and see” approach, according to TechCrunch.

But plenty of cash is still available, and many startups are raising funds. The ecosystem is experiencing a remarkable influx of funding, with more new venture capital funds emerging than ever in history. It is easy to see how much money is available for promising startups, with over $580 billion in dry powder waiting to be deployed. However, demonstrating your company’s full potential is even more crucial, and preparation is key. As we start Q3, we have a list of 15 startups from our alumni community who raised investment in Europe and beyond just in 2023.

Compared to their previous round and the experience of many other founders, Brittany told us QFlow’s fundraising process went very smoothly this time round. According to her, two key factors contributed tremendously to this:

The most basic and critical one: the business is in the right place, and it has successfully hit all its targets

Brittany’s preparation was extremely careful, from planning the whole process before going to market to building an exceptional investor pack and communicating their strict timelines.

Let’s dive in.

Planning and Fundraising Preparation

A few months after going through the Fundraising Bootcamp in October 2022, learning about the process, and rewriting her deck with our team, Brittany used the end-of-the-year holidays to plan and strategize the next steps in their fundraising plan.

The process was much easier this time, partly because we planned a huge amount of legroom, and the Fundraising Bootcamp was really helpful in helping us understand how good planning could look. Even stuff that is often overlooked, like being fully prepared before even entertaining any conversations with investors.

As the sole responsible for raising funds for her company, Brittany designed everything they needed following Bootcamp’s strategy: from exact timeline to the right list of investors, prepping their investor emails, building the perfect data room and all the details on assessing and approaching interested funds.

During the planning stage, Brittany Harris also decided not to disclose their valuation expectations upfront, as advised in the programme, instead allowing investors to determine their pricing.

Selecting the Right Investors

Brittany drove the process timeline from the get-go, setting clear expectations and dates to potential investors. All targeted investors were informed of the exact process timeline via an investor update email one month before the round opened in January.

Reflecting on their previous round, she recognized the importance of avoiding wasting time and effort on engaging with investors who were not a perfect fit for the business. This time, Harris focused solely on highly targeted investors, following the guidance of the Fundraising Bootcamp. By targeting only suitable investors and investing in her stage, sector and geography, she minimised wasted time and resources on unproductive engagements.

Evaluating investor fit and using the Pyramid of Priorities to categorise them into tiers made everything more straightforward, separating investors based on their alignment with the company’s vision for the future.

Comprehensive Data Room

Bootcampers know how a well-structured and comprehensive data room facilitates due diligence and enhances investor confidence and trust in the startup.

Brittany dedicated the end-of-the-year holidays in 2022 to building QFlow’s data room in full detail, taking advantage of the quieter period to focus on the planning stage.

Their data room gave investors everything they needed to understand Qflow comprehensively and to conduct due diligence. It served as a centralised repository where investors could access essential documents, financial information, market analysis, and see other relevant materials necessary to facilitate the deal.

One of the main feedbacks we had from investors was, “Oh, this is the best data room I’ve seen in years”

Driving the Fundraising Process Timeline

In a market that is dragging its feet, QFlow oversubscribed its round in just four months, two months earlier than the market’s average. Harris believes the strict timeline was the single most important asset that helped them close their round so fast.

Using an investor update newsletter, Brittany communicated the various stages of their fundraising journey with all investors from the get-go. She gave a heads-up about the start of their round about a month before the opening date, detailing the exact dates when they would open the data room, meeting availability, and a clear deadline for entertaining term sheets.

Along the way, additional investors were recommended by the ones she originally had approached. Still, QFlow did not extend its timeline. Hence, investors who came in late had to catch up if they wanted to participate in the round, staying fair to others who had already committed to the original schedule.

In a resolute move, Brittany dismissed some investors who disregarded her (well-communicated) fundraising timeline. When an investor expressed their intentions to submit a term sheet in June, Harris responded, “Don’t bother; the round will be closed by then.”. Despite recognizing the potential value these investors could bring, she couldn’t help but question their dedication. “We clearly communicated the timelines, so why didn’t they take it seriously?” she pondered.

Much of what we discuss during the Fundraising Bootcamp revolves around driving the process timeline, and QFlow is the perfect example of how this works for the best. Investors are the only ones who benefit from dragging a decision, not only because desperate founders accept worse terms, but also to see if other investors join first, who might lead the round, etc. In QFlow’s case, the timeline was set from scratch, and investors who did not take it seriously missed their chance.

Valuation Strategy

Following our Bootcamp’s recommendation, the team let the investors price the round rather than disclosing their valuation expectations. As is often the case, the first two term sheets they received didn’t really come close to the number they expected.

By tracking access to her data room, Brittany could tell those investors hadn’t spent enough time analysing the business, which was a red flag. However, knowing that the market has been tricky, she couldn’t help but wonder, “Is this all we’re going to get?”. Taking a step back, she discussed the situation with their board and, together, they decided to stay put:

“We considered [the term sheets], took them to the board, and said that we were not happy with it, but that we knew that the market was really bad at the moment. Since we had runway until the end of the year, we decided with the board to see what else we could get.”

It will come as no surprise that having enough runway changes everything, from how you position yourself, to your pitch, to what you’re open to accepting. In QFlow’s case, they had room to juggle and could afford to ask, “Is this going to help the business get where we need it to go?”. And with those two initial term sheets, the answer was clear.

They waited patiently, and a more reasonable valuation arrived in mid-March. If the first term sheets came from funds that did not fully align with QFlow’s plans for the future, this time around, the better valuation came from a more specialised fund, one they could benefit a lot from having on the cap table.

Once QFlow accepted the term sheet, Brittany spread the news. This is a deliberate tactic we share in the Fundraising Bootcamp to cause FOMO and leverage the interest of other investors, also serving as a friendly reminder that the funding round was drawing to a close.

With a good offer in hand, they began finalising the round following their originally proposed timeline. Despite their initial target of £6 million, QFlow ended up closing an oversubscribed round, raising £7.2 million.

Divide and Conquer

In contrast to their previous round, Brittany and her co-founder, Jade Cohen, had a different approach in the separation of tasks. In their first round, they attempted to handle fundraising responsibilities together while also working on the business, which ultimately proved to be an almost impossible task. Recognizing the need for a dedicated focus, they decided to divide their responsibilities this time around, which was a game-changer.

With Jade handling the business operations, Brittany could fully immerse herself in the fundraising process without being weighed down by other responsibilities and while tapping into her strongest skill set. It created a supportive environment where Brittany could dedicate herself entirely to fundraising, ultimately leading to a brilliant funding round, while Jade managed the operations and made sure to shield Brittany from the day to day challenges of the business.

Lessons Learned from the Fundraising Bootcamp

If we were to summarise Brittanny’s four crucial takeaways that influenced her process:

Timelines are Key: Setting and adhering to strict timelines ensured investors understood she meant business. From day one, she was straight to the point with investors: the exact date they would start their fundraising process, when the data room would be open, meeting availability, and when they would entertain term sheets.

The Power of Preparation: Harris prepared the whole strategy for the round before going to market Everything was defined when they opened the round. Their detailed data room and documentation pack impressed investors – Brittany was kind enough to share the structure of her data room in our exclusive community for Fundraising Bootcamp alumni. This community is where we aim to build a valuable platform for founders to seek guidance, offer assistance, and benefit from the collective wisdom of their peers.

Trackable Pitch Decks: Leveraging tools like Brieflinks, Brittany and her team could see what investors were most interested in their pitch deck and data room by monitoring the time spent on each section and then be able to focus on those points when having their meetings.

Trust Yourself: Saying no to the first two-term sheets they got took a lot of confidence. Harris was adamant about the need to trust in her deep understanding of the business and its potential. “Questioning yourself is extremely important, but sometimes you just need confidence in what you’re building.”

“If you got a business in a good position, reaching its targets, that’s really interesting [to investors]. We hit all the metrics we set out to. It wasn’t a question of “Can you do it?” anymore because we were already doing it. It was a matter of “Do you believe in our vision for the future?”.

Listening to Brittany share the journey of QFlow’s Series A fundraising round made us extremely proud of her efforts. In a truly challenging market, Brittany closed an oversubscribed round in just four months from European and US investors who are the perfect fit for the startup’s future. QFlow’s Series A story sums up so much of what we talk about in our cohorts, and hearing about its successful outcome is truly inspiring!

With the funding secured, Brittany and her team now have the opportunity to focus even more on decarbonising the construction industry. We’re excited to see what the future holds for them!

Startup founders, if you thought the fundraising landscape was challenging before, the past few months have been getting even more brutal. As desperation and fear rise, investors come back with not-so-new term sheet clauses designed to benefit them and leave founders at a disadvantage.

These term sheets aren’t new. I survived three different crises, and (sadly) little has changed: dirty terms have been a part of the VC landscape for a long time and seem to re-emerge in every downturn. Unsurprisingly, they benefit investors by overprotecting them on the downside while ensuring they also get more prosperous outcomes, while founders get harsher terms and usually a higher risk of getting crushed.

Let’s get it straight: VC funding is the harshest form of capital you can raise. You can criticise all you want, search for alternative funding sources (recommended: RBF is on fire, for instance), hope for the best, or learn how the game works and the different terms you’re likely to be offered today.

My worst scenario: investors playing the clock.

Most founders don’t even realise they’re being played. Investors slow down the pace of the entire funding process to a grinding halt, add steps, bring in more people, more due diligence, more checks, more…everything. This typically ends with founders running out of cash, getting desperate and accepting any terms by then – simple equation, accept this, or your startup dies. Experienced investors play that game oh too well, and most founders don’t even realise it until it’s too late.

The only tool you have is information. You must define your timeline and avoid the clock game, set the minimum (and immovable) terms, negotiate assiduously, and ensure you always have enough alternative investors as plan B. Good investors exist but are rare – it’s your job to find them and set the terms straight from the get-go.

Without further ado, here are some term sheet clauses you should be expecting to deal with in moments of crisis:

Full-ratchet anti-dilution

Pro-rata anti-dilution is common. It’s designed to protect investors from a later “down round” (the company raises money at a lower valuation in a future round). I know it doesn’t exactly make your investor a true partner, there for you, for good and bad times as they claim to be, but… that’s another topic. Down round? You send them some of your shares to compensate for the loss between the valuation they came in at and the next round. However, it’s a typical clause, so expect it.

The dirty version is the “full ratchet” version, and it’s propping its ugly head up again during these hard times. And you must not accept it. To keep it short: instead of sending some of your shares to the investors to compensate for their ‘lost’ value, you send them shares for the entire amount invested. No pro-rata. It’s 100% of the investment you return from your shares (only).

It’s a famous clause, as it has wiped out entire cap tables, leaving founders with nothing (I mean it: zero per cent) at exit time. Now you know.

If you want the entire math of the anti-dilution clause and how it turns ugly, head over to this great article by Tim Wilson, from SeedCamp.

Multiple Liquidation Preferences

Multiple liquidation preferences is a clause that gives priority to the investor when the company is being liquidated, guaranteeing that they will get paid first – before everyone else, including founders and previous investors.

This clause can (and will) reduce the money founders and team receive, usually significantly, especially if the exit price is moderate (say £50m – £250m, the vast majority of exits here in Europe).

Today some rogue investors will try and demand a 2x liquidation preference (we heard of a 6x already!), meaning they’ve doubled their money before anybody gets one dollar out of the company sale proceeds.

The dirty trick: piling these preferences (two or three investors in each round, times 2 or 3 funding rounds) and adding some interest on the funds paid out to founders. Result: even with a £100m-200m value at exit, founders still leave with nothing. It’s crazy.

This one’s also known for being pushed today. And for taking out most (or all) exit proceeds, leaving founders with little…or nothing at all. Investors usually have an option: get a fixed, guaranteed multiple of their investment by the end of a period or convert their shares into common shares and sell them alongside the founders/team.

With the participating preferred, the investor gets to “double dip” by not only getting his preference but also sharing in the remaining proceeds, as if they were converted into common – further reducing the amount paid out to those who actually built the business.

Milestone-based tranched equity rounds

Few clauses create as much uncertainty for a startup as this clause. Milestone-based tranched equity rounds are sold by investors as a “reward” method, in which funding comes in instalments based on certain milestones being reached. Miss a milestone, and your next funding tranche evaporates. So founders, unsure of capital being available, play small hands, don’t invest in growth, don’t take risks, don’t hire the best staff or spend for growth. They hold back and miss their targets a lot of times. Self-fulfilling prophecy.

The venture category is about giving a company and its team the resources to execute, not starve them of oxygen and limit their growth. If your investor doesn’t believe you can achieve it, they shouldn’t invest, and you shouldn’t take them on, period.

This is a tiny sample of nasty term sheet clauses you should know, expect, and learn how to negotiate. There are many more, and at least eight that will rip you off, guaranteed. If you don’t want to be the next victim, join us.

This article might sound anti-VC, and I’m 100% not. I decided to write this to remind founders that without a proper funding plan and process, you can get squeezed, offered unsavoury terms and must have the knowledge to avoid the extra pitfalls.

Don’t blame VCs. Their job is to produce enough returns to protect their investments and investors. Don’t argue, you’d do the same thing if you were in their position. Learn, prepare and get ready for it – what they seek is not what the media tells you, so face the harsh realities and be the one who gets a fair deal.

Negotiate smartly, discuss everything with your network and fellow founders, ensure you’re not making textbook mistakes and know every clause of the deals on your table. Times are tough, and having support from a community of startup founders and experts is more important than ever – feel free to join ours.

Here’s what you can do as a founder to avoid being the victim of investor scams.

As CEO or founder, it is your responsibility to find suitable investors for your business. And just like any other group of people, there are good and bad-intentioned people, so before you sign anything, be mindful of who you are getting into business with. Unlike a civil partnership, there’s no divorcing your investor/s.

It’s always been challenging to raise funds, but as the VC market heads south, it’s getting harder to meet (and get funds from) top-name VC funds and reputable investors. And that lack of good investors gets filled by – you guessed it – rogue ones. Nothing new, they have always been lurking around the corner, but when capital was plentiful before, it was easier to avoid them.

We’ve talked about how not all investors have your best interests at heart before, so we decided to create a quick guide of things you can do (besides following your gut), so you’re not the next victim of an investor scam. Let’s dive in.

Common investor scams when raising funds for your startup

Scammers have existed for centuries so the list could be extremely long.

Loan sharks

The most commonly reported scam in the startup world nowadays is zero-equity loans. They have incredibly onerous interest rates, short periods before the first payment, high ‘activation fees’, expensive exit premiums or penalties, and also grant themselves warrants available (at their option but not their obligation) for years. Hence, they get the right to invest in your business once and only when it’s flourishing without investing. Many also have complex convertibles, granting themselves rights without investment, bonuses down the line, or even full ratchets.

Service Providers

We also see many fundraisers acting as investors, getting your entire doc pack and confidential information with (of course) no NDA, offering to ‘invest’ a portion of the commissions or fees they charge you for arranging investor introductions. Some may also kindly blackmail you; they could take your information to direct competitors claiming they know the market so well and have “market intelligence”. There’s no cash offer, they’re just selling their fundraising services, usually at above standards and occasionally at exorbitant retainer and success fee rates.

Term Sheet sharks

Sometimes, however, you have actual investors offering you cash – but with some exotic clauses, claiming it’s “market standard nowadays”. Just so you know, there is no standard term sheet.You get the terms that you negotiate, period.

If you’re new at this and need a base template, use the British Venture Capital Association’s. It provides enough protection for investors and no nasty surprises for entrepreneurs. You can download master templates here. There are some other good ones too, in plain English, not legalese, that you get during our Bootcamp.

Examples of some nasty term sheet clauses they’ll try their luck with – there are plenty more, that’s just a few, for illustration purposes:

(Very) short-term exercise periods. Employees only get a few weeks to convert their fully vested options into shares. The later the stage of the company, the higher the value of shares. Good luck finding several million in cash with no plan to exit or IPO. So options don’t get converted and return to the company, giving the company’s shareholders a bigger slice at no cost.

Full ratchet anti-dilution. They invest X million into your company at a valuation of Y million. Should you raise at a lesser valuation in the next round (even by just a dime!), you hand them back the entire investment. That’s how CEOs and founders of companies going public end up with 0%. Yes, zero. Tons and tons of famous companies going public stripped the founders.

Once again, be extra careful about the term sheets that can completely destroy your business. If you want to know the other terms and tricks that can strip you out even if the company does well, I highly recommend you join a Fundraising Bootcamp – we have a whole module just for this. It will save you from disaster.

Funds…raising their own funds.

Every five years or so, funds also need to go fundraising, and they need a few good things in their marketing materials to have a chance at attracting good-name LPs. One of these must-haves is a list of hot deals, available now.

That’s you.

They’ll tell you the fund is “almost closed”, “partly closed”, “‘fully committed” and other BS. What usually happens: massive delays, especially for new or first-time fund managers. LPs aren’t backing new ones but are investing more in big-name funds and experienced managers.

There are a lot of investor scams going on right now, and it’s not pretty. Some LPs are starting to call out phoney VC claims. Don’t fall for the PR clickbait.

How to protect yourself from investor scams

Short answer: data, data, data.

Most perpetrators are very good at pitching their products and hiding the truth. Their ability to provide hard data is typically nonexistent. So check the small print: skip the general questions about their services, benefits, comparisons, or advantages, and instead ask pointed, precise, detailed questions.

Few examples:

With a 10% inflation applied, what’s the total cost of their loan? Any admin fees or international rates/transfer charges? Account setup or termination charges? Early termination or repayment fees?

Ask them to show you a monthly repayment graph for £X over a period of a number of months

On a fully diluted basis, what’s the total ownership granted to you if we sign up for your service/s?

Ask them to build and show you a cap table with their investment and ownership in it after this round, the next round and the round after that – on a fully diluted basis.

Fake investors: ask them about the last three deals they invested in, including the name of the CEO. Call them and ask for their terms, LP names, and Fund Reg details.

So, what can and should you do? 1. Make a hard pass. They sometimes use your name or contacts to connect to other CEOs. 2. Disconnect them from all your social networks 3. Inform your peers and network. Founders trust other founders.

Scammers are true innovators

The short of it is, as cash gets harder to secure, the terms on offer are about to worsen. So be warned. Prepare for the extended due diligence you didn’t need to do only six months ago, and don’t despair: once you’ve done two or three, you’ll smell a rat before you even talk to them.

Remember, the above is just for illustrative purposes. Many other investor scams are going around, and scammers are great at innovating. So trust your gut, ask your founder friends, reach out to experienced advisors (hello!) or just join us at the Fundraising Bootcamp to become a pro at fundraising. You still get a gang of successful founders and advisors to get you there safely.

Whenever you’re ready to move forward with a trustworthy investor, you should also do your due diligence before signing anything. I know it sounds like a lot of steps, but it’s your job as the CEO to ensure your company’s and your team’s future. Exhaust all options and guarantee your investor wants the best for your startup.

There you go – here are some high-level insights. There’s a lot more, but that is long enough already. For more, you know where to find us.

There’s no undoing or divorce with investors. You’re in for the long haul, so make sure you due diligence investors before you go all in. Here’s how.

We’ve all heard the horror stories of mismatched VCs and startup founders/CEOs – the politics, bad blood, failed relationships, or broken trust that kills good businesses. Is it really that VCs are bad people? Or is it just that not some people shouldn’t work together?

VCs will assess who you are as a person, how you operate and interact, and how able you are to attract stellar staff, partners, other investors etc. Early on, their only focus is on the quality of the founding team.

Unfortunately, founders often ignore the basics: you are about to commit to these investors for 7 to 10 years, sometimes longer, and you cannot divorce them, no matter how bad the match may be. Running thorough due diligence on investors is a must. As the CEO, it’s your responsibility to assess and find suitable investors, and yours only.

When starting to negotiate with VCs, it is far too common for founders to rely extensively on their gut feeling and “basic instinct” and decide not to due diligence investors. Yes, your runway is running short, and the cash/offer is attractive, but if there’s no match? No deal. Period. There’s nothing worse than discovering post-round that one of your investors is a bully, monster, liar, egomaniac, etc. Sadly, there are quite a few – it’s your job to find the outstanding ones.

Everyone has different needs. When I was raising, for simplicity’s sake, mine were: the investor should be (1) a team player, (2) a good listener, and (3) true to their word. They should also be willing to lean in and help out when needed.

You must run thorough due diligence on investors and ensure they are a good fit for you and your company. Of course, gut feeling helps, but it is nowhere near enough.

Here are a few practical, no-BS tips on how to do it thoroughly and efficiently. Let’s dive in.

Check with other founders/CEOs

You’re lucky: Tech/Digital is the most progressive industry, and CEOs share all sorts of information, tips and recommendations, so make use of it. Other industries are very jealous of ours for that.

If you’re looking for information on a potential investor, chances are good that someone in the tech community has already worked with them. Ask around – you’ll likely find more information from your peers than anywhere else.

Initially, some CEOs may be shy. You can get them to talk by asking about specific events, not about them or their character. Practical questions work very well.

“Does s/he always read the board pack well ahead of the board meeting?” “Do they add a topic on the agenda or go with yours?” “Do they often cut you/other board members off?”

You may ask a VC for references too, but I find that you only get to speak with their favourites and best cases, so that’s useless. I usually call CEOs directly – if a VC has an issue with it, why? What do they have to hide? It might be a red flag.

If possible, arrange to meet personally rather than over the phone, as this allows you better to interpret their views through their facial and body expressions – and they might feel more comfortable sharing what they really think. Take note of how they describe the VC, too. Do they “always knows best”? Do they invent knowledge or hard data to hide their lack of understanding?

After 3 to 5 interviews, you will start seeing a good or bad pattern. That would be around five 20-minute chats or coffees, that’s it. Well worth the investment.

If you don’t have a community of founders to ask about investors, join ours. It’s made of 180+ founders, covering 24 countries and with hundreds of VC experiences from seed to IPO.

Check Glassdoor and the others

If you’re a terrible person, you’re probably also a terrible boss inside the VC fund. That’s what the staff thinks, anyway, according to Glassdoor.com. There are platforms where founders can anonymously share their experiences dealing with investors, such as Landscape VC and VC Guide. Yup, anonymity is a b*tch for monsters. 😉

Of course, you should always be wary of overly negative posts – the people with the worst experiences always shout the loudest. But it’s usually worth digging into it, you’ll find some golden nuggets most of the time.

Check their depth

I love a fantastic tool out there called Shipshape.vc.You can use this venture capital search engine to find posts from specific people and what topics and tags they use frequently. Try it for yourself, and you soon discover the investor’s real interests vs. what they claim to seek/know/invest in and how much they know about a topic or your sector.

Check their personality

Investors are very polished, broad-smiled, professional, and even charming when you meet them in their office. That’s because it’s a fixed-frame environment. Well rehearsed and coordinated, with each plant and wall picture placed perfectly. They’ll deliver their lines, act and sound the part. And most of the time, it’ll be fake. An actor, not a true person.

A simple trick I’ve been using extensively is to take them out of their stage. A walk, arduous hike, lunch, dinner, or simply drinks are all excellent options.

Watch how they interact in the real world; you’ll see their true character and personality in minutes. Do they walk in front of you all the time? Are they focused on you or their phone? Do they take calls or write a text mid-conversation? Do they open the door for you when you arrive? Do they treat service staff politely?

My favourite one is spilling your glass of water on the table “by accident” and watching how they react. Are they immediately upset and lack self-control? Do they help out with cleaning up? Can they focus and resume the conversation quickly, or did they lose all attention? You will notice changes in their attitude, focus, character, and engagement in real-life situations.

Why do this?

Because you see the real person under stress – and you will have loads of stress, that’s the 100% guarantee I can give you, during the 7 to 10 years you’ll build a business together. So better still know they re/act when the going gets tough. This is a much better indicator of their true personality than their office act.

Check their collaboration skills

Once convinced that your company has potential, good investors will gladly spend a few hours with you and your team to work on a specific, strategic issue. What does success look like in 5 years? What’s the cost of us reaching this amount in revenue within three years? What does the team look like to reach its full potential in four years? And so on.

A good investor can help you flesh out your vision and develop realistic goals and targets. They will also be able to give you advice on what to do (and what not to do) to help your company reach its full potential.

Good investors help and poor investors state. Easy to find out whose which, just use a whiteboard session.

Ask the investor directly

The list is infinite, but some of my favourite ideas include asking them a few questions that can say a lot about their behaviour. Pay attention if they take the blame for mistakes, if they share the burden with other founders or if, in their minds, they’re always fault-less. Some topic ideas:

1. The worst CEO they invested in – see if they get personal or stay factual

2. Worst challenge they experienced with a founder

3. What process they used to fire/replace a founder

4. Biggest disappointment with a CEO post investment

Take notes, stories and anecdotes will cross over with other CEOs’ own, so you can check what’s true from BS.

Final test: Psychometric test

At that point, you should have formed an image of this investor in your mind. If everything checks out, ask them to do a psychometric test. Most investors already have one, so no extra time or work is required. If it is their first time, it takes less than 45 minutes.

Make it a two-way process; many VC funds also ask founders to do theirs as well. Tell them it’s not a test, and there are no right or wrong answers – you’re simply assessing your future.

“I see this as a marriage, and we all know that nobody’s perfect. Expectations will be realistic if we know our strengths and weaknesses in advance. I’m trying to build the strongest team possible.”

The tests won’t tell you everything you need to know about an investor, but they can be useful. 45 minutes may seem like a lot, but it’s a small time investment for such a long commitment.

Due diligence investors might sound like a lot of work, but for the sake of your company and team, there’s nothing more important than this in the long run. You will never jump through this process when you realise how detrimental a bad relationship can be for your business.

The right VCs will understand and support the importance you put on this. Take your time, do your own research and ensure you are compatible with your potential investor. In case you’re not sure they are legit, we wrote about spotting a rogue investor and term sheet clauses that can destroy your business – check them out.

You read the story of the one in a million; the startup that immediately turns into a rocket and IPOs in 7 years. That’s the dream, right? But in reality, when raising venture capital, not even 10% of all startups make it.

The great majority, however, go through something more like this: have a great idea, check. Find a talented “team” of believers, check. Build a great product, find your market segment, screw up, learn, iterate, screw up again, learn more, iterate more, find something that works, double down on that, lower your CAC, improve your conversion metrics, find a “sweet spot” and start feeling good. You then go to the market to raise money and… crash out.

Times have become more challenging because of the recession (we even discussed this in a recent session) but irrespective of the time, keep this in mind: when raising venture capital, you will get rejected. Many times. So you might as well be rejected for the right reasons, not for things you could have easily avoided.

The best thing you can do to increase your chances of raising Venture Capital investment is to avoid the textbook mistakes startups make.

Common mistakes when raising venture capital for a startup

Is your business a VC business?

VC funds need huge (read: huuuuuge) returns to make it worth their while. That means they aren’t interested in anything that is not supersized in financial returns.

So your dream business that does $5m per year in sales? Sounds like a nice business, right? Well, not for VCs. As a median SaaS business with a valuation of around 30-50x revenue, $5m x 30-50, or $150-300m. VC firms own 20%, so $30-60m. If they invested a total of $25m for that 20%, that’s a nice multiple on capital, but nowhere near where they need to be.

That doesn’t mean you can’t raise investments or that you don’t have a fast-growing business, it only means that your business won’t be interesting for venture capital firms.

You’re not approaching investors strategically

The game should be played strategically if you want to win. Not all investors are equal – and you should prioritise them accordingly. If a good investor decides to invest in your startup, other investors will feel that they are missing out on something, rushing to try and close with you, too.

Choosing who to approach first – and how to approach – is essential when raising venture capital. The best way to do that is using the Pyramid of Priorities, explained in detail here.

You go to market when you need cash

The press and everybody will tell you that raising funds is quick, while the hard data shows you precisely the opposite. If you’re raising funds when you already need cash, you’re raising at the worst time possible.

We’re big fans of DocSend’s analytics of pitch decks, and looking through their hard data and reports, it’s easy to learn that an average round is 23 weeks. At the Fundraising Bootcamp, we suggest that you have at least (at least!) 6 months of financial buffer when you start your process. Plan accordingly.

Your pitch is poor

During pitch presentations, startups talk nonstop about them. Instead of focusing on what matters to investors, they constantly talk about their team, customers, growth timeline and all details about themselves. What’s in it for them? What VC investors care about more than product, features, or anything else is how they will get 100 times the return on their investment.

Investor decks are very calibrated, and we know what’s there. If your deck doesn’t have the minimum data points expected by investors, commonly found all over the web, that’s your fault. Some VCs are so straightforward they add those details on their website, so check first.

You’re not ready yet

There is no such thing as a casual chat – if you meet an investor, even in a casual setting, and the investor thinks you are “alright” you will never get an invitation to a proper meeting. That informal meeting is your last chance to meet that person. If you’re not ready to go all in, you’re wasting your only chance.

You haven’t dedicated enough time to raising venture capital

Seed rounds take 12.5 weeks on average (and much more, in many cases), at least 58 investor contacts, and 20 pitches. We see too many part-timers juggling product development, customer sales, and fundraising on the side and think that’s enough.

Fundraising is a full-time job. Doing a little bit on the go is even worse than stopping entirely.

Your idea doesn’t have a market

The world is full of tech solutions looking for market problems. Even at an early stage, founders insist on Product-Market fit.

“Make something people want” is Paul Graham’s quote that became Y Combinator’s motto.

If your product is still not usable, prove the niche, the need, the request, and how your idea is supposed to serve all this. Doesn’t matter how great your product is – if there’s no audience, you don’t have a business.

Having hustled for years and advised startups/scale-ups for many more, I have become jaded by the sheer amount of the same mistakes – it wastes everybody’s time, both founders and investors, and they can easily be avoided. Worst of all, now you have experts and self-acclaimed gurus giving free and terrible advice to founders, making them follow the hype and not learn about the practicalities of fundraising successfully

In 2020 I decided to solve it myself and co-created what we call the Fundraising Bootcamp today, an investment readiness programme that just works. I know the list is long, but it could be way longer. There are infinite mistakes, spoken and unspoken when it comes to presenting your pitch to investors. If you want to be genuinely prepared, join one of our next programmes.

We all know fundraising is quite complicated right now. It’s not the real crisis the press will have you believe, but it’s slow and arduous, even more so.

Now something nobody tells you: not every investor has your best interest at heart, and we should be talking about that.

I know it well, as I suffered it myself. As a CEO, I lost everything once. Millions of euros raised, a team who had invested their lives, years of hard money, everything: lost. My time, energy (possibly my marriage) and hard work included. Wiped out.

The culprit? A seemingly innocuous clause in our term sheet: Minority Veto Rights.

As it sounds, it allows minority shareholders/investors exceptional rights, bypassing the standard Shareholders Agreement. It allowed a rogue investor to block further, much-needed funding. He also locked two buyers from acquiring the business (which would have made everybody very happy, including the said investor) and, worse, allowed them to reset the company’s valuation to zero (also named a cramdown), which led us to lose the entire founder team, staff and the other investors their lives work.

Unfortunately, that’s not uncommon. It’s so easy to fall into a trap without knowing it, and a recent CEO who joined our Fundraising Bootcamp shared a story remarkably similar to mine. We even have a module named “nasty term sheet tricks” which discloses those tricks that will 100% kill you, and how to negotiate them out.

Many CEOs are first-time founders with zero or little fundraising experience, while investors do deals day in and day out. Fundraising is challenging at the best of times – add to that the number of unscrupulous and fake investors out there, and you could be in for nasty surprises. There’s so much that can go wrong before it goes right.

I urge you to find your gang of experienced founders, mentors, lawyers and investors to help you navigate the process before you even consider signing anything – or you can join ours.